For socially conscious investors, the idea of “investing from the heart” sounds appealing. The phrase conjures up ideas of only supporting companies whose ethics and values align with our own, and avoiding those engaged in businesses we find distasteful, dangerous or morally repugnant.

It’s true that personal finance is primarily an emotional, rather than logical endeavor (although plenty of analysts would have you think money subjects are entirely relegated to the cold, calculating left brain).

The notion of moral or ethical investing has its roots in the 18thcentury and conceptually is credited to John Wesley, founder of the Methodist Church. Wesley preached that the use of one’s money should not harm another person. More recently, mutual insurance company, Friends Provident, moved socially responsible investing from the conceptual to the practical when it launched The Stewardship mutual fund in 1984.

The U.K.-based fund avoids investments in companies that don’t meet specific ethical standards or that “harm society.” According to company literature, Friends Provident strives to invest in companies that “make a positive contribution to society.” And, its managers seek to encourage better business practices through “shared ownership and dialogue”. Interestingly, the Stewardship Fund’s three principles are the lynchpin of what is today referred to as ESG Investing.

ESG stands for Environmental, Social, and Governance, which according to the Forum for Sustainable and Responsible Investment, will lead to “a more sustainable and equitable society” if these three principles are “meaningfully assessed in all investment decisions”.

In other words, the thought process goes, if investors pay attention to non-financial factors, then we’ll all live in a better place.

That’s where the notion of heart-centered investing begins to make sense. It doesn’t mean casting aside analytics entirely.

If your intended investment objective is to have a cleaner, fairer world, then you really want to screen your investment candidates for environmental and social criteria, using a combination of quantitative and qualitative metrics.

Things like a company’s track record on polluting or contributing to landfills would be important to you. Likewise, a company’s position on child labor laws, prison labor laws, or slave labor laws would also be important investment screens for you.

Governance is a little different, however.

A company’s governance is its structure for determining practices by which the firm is run. These principles apply to long-term strategic vision as well as day-to-day tactical execution. Governance must weigh the interests of various constituents, including customers, workers, shareholders, vendors, government agencies and the wider community.

Whatever your intended investment objective, corporate governance is critically important. So, it really doesn’t matter if you want to use your dollars to save the planet or to make as much money as possible. The only way that you can be confident that an investment is going to deliver on your objective is if its management is honest and ethical. We’ve all seen how dishonest management can take down a company. Enron or WorldCom, anyone?

Corporate governance is vital to the transparency required for an investor to believe the numbers that a company reports (whether they are earnings per share or size of carbon footprint). All public company officers need to be accountable to shareholders, employees, customers, and suppliers. It may sound naive and chortle-worthy, but honesty and integrity are the keys to making the whole financial system work.

That is not the case with the other two principles pertaining to the environment and social factors. While they may help identify companies that are good stewards of the environment or ones that benefit global society in a measurably tangible way, they don’t necessarily lead to better investment performance.

Don’t get me wrong. The idea that one’s investments ought to mirror his or her morals and ethics is laudable. But, investors should not be mistaken. There is a tradeoff to be made. In most cases, that tradeoff is between value and values. Funds offering socially responsible investment (SRI) themes do not provide investors with comparable returns to unmanaged index funds that track the Standard & Poor’s 500 index – simply because these funds are, by definition, actively managed and do not track that benchmark!

Nevertheless, socially responsible and sustainable funds are a fast-growing investment category.

According to the Global Sustainable Investment Alliance the rush by investors into socially responsible, or SRI, products has exploded. At the end of 2016 there were more than $22.8 trillion invested in “sustainable investment assets.” This represents a growth rate of better than 25% since the end of 2014. So, clearly, there is demand for this type of investment. But are they profitable for investors?

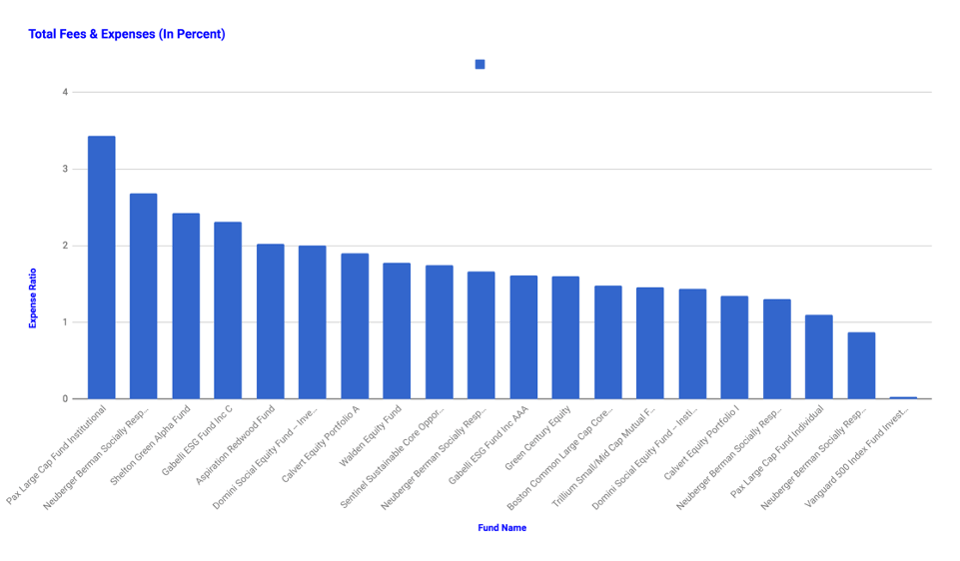

To be sure, they are very profitable for the institutions that create, promote, and manage the funds. After all, nothing proliferates on Wall Street if it doesn’t make money. According to Bloomberg’s Environmental Social & Governance (ESG) Data Service, the average fees and expenses for SRI funds investing in domestic equities and benchmarked to either the S&P 1000 Index or the S&P 500 Composite Total Return Index cost investors an average of 1.785% per year.

That may not sound like a big number, but to put it in context: Total fees and expenses of the Vanguard 500 Index Fund add up to less than 0.30%.

Morningstar has done extensive research illustrating the degree to which expenses take a bite from investor returns.

As the chart below illustrates, fees vary widely. Sadly, most people are unaware of the amount a fund manager is pocketing before the investor receives his or her return. That’s true for all investment products, not just those carrying the label of “socially responsible” or “sustainable.”

That many funds focusing on socially responsible investment themes are expensive shouldn’t be a big surprise. The investment business is replete with fancy, fashionable ideas that are good for the investment manager and not always so great for the individual investor.

The greater issue with SRI funds is that the criteria used to make investment decisions is very subjective. By way of example, let’s look at one of the oldest mutual funds available in this category, the Domini Impact Equity Fund (DSEFX). The fund has been in business since the mid-1990s. Because of its age, one could argue that the the Domini Impact Equity Fund makes a pretty reasonable proxy for an SRI index.

The fund acknowledges that its socially responsible investment screens are a bit open-ended. Their Social and Environmental Standards state that “Domini may determine that a security is eligible for investment even if a corporation’s profile reflects a mixture of positive and negative social and environmental characteristics.” That’s not unusual; other fund families also use sustainable and socially responsible screening mechanisms that allow for some wiggle room.

Many fund companies use the “carrot and stick” approach, as well. For example, a company may be rewarded with investment dollars for making progress on issues such as greenhouse gas emissions, but punished by withholding of funds if progress is not made fast enough.

But, what have these screens done to create value for the fund investor?

From the beginning of 1995 through the end of May 2017 the Domini Impact Equity Fund offered investors a Compound Annual Growth Rate (CAGR) of 8.47%. Over that same period of time, investors in the unmanaged Vanguard 500 Index Fund enjoyed a CAGR of 9.66%.

So, for investors whose objective is simply to grow capital, the hands-down winner would be the passive approach offered by an index fund.

But that doesn’t mean that investors trying to match their investment objectives with their values can’t make money. They can. But, as with all active strategies, returns may not be optimal, largely due to expense ratios and the vicissitudes of stock-picking.

Ultimately, socially responsible investment screens that zero in on specific industries are akin to emotion-based stock picking. As long as the investor is aware that he or she may be giving up some degree of market return, then these funds may be a good choice.

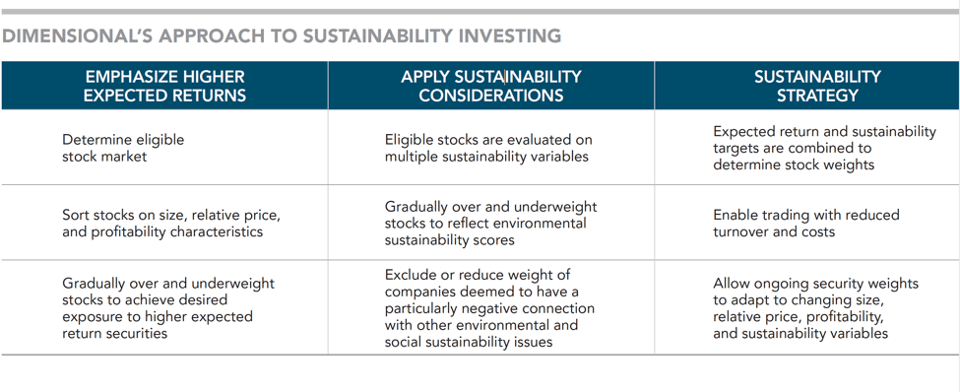

It’s important to note: It’s not a foregone conclusion that investors must sacrifice a big chunk of their return in exchange for a portfolio that’s aligned with their values. For example, Dimensional Fund Advisors’ approach to sustainability seeks to address the issues important to investors while offering broad diversification and focusing very deliberately on higher expected returns.

According to DFA literature, “To meet this goal, sustainability considerations can be integrated within a robust investment solution that pursues higher expected returns through increased weighting to securities with smaller market capitalization, lower relative prices, and higher profitability. Dimensional’s approach can offer investors the ability to pursue their sustainability and investment goals simultaneously.”

Rather than picking and choosing industries and stocks, Dimensional begins with a strategy of broad diversification, encompassing the entire investment universe. From there, sustainability screens are applied “based on data that allows for systematic evaluation of companies according to multiple environmental and social sustainability variables.”

This graphic illustrates the Dimensional approach to screening.

In summary, it’s not necessarily the case that socially responsible or sustainable strategies are more expensive than others. Each investor must decide for him- or herself whether it’s worth paying some extra money for the “stick” approach – in the form of expenses or opportunity cost – to filter out certain industries, or whether the “carrot” approach of pressuring firms in all industries to improve sustainability metrics is preferable.